| Capital at risk. All investments involve risk and investors may not get back the amount originally invested. |

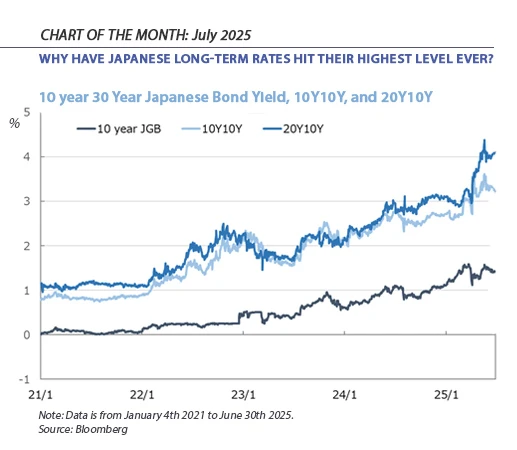

This month we focus on the recent surge in the Japanese interest rates, where the rise in yields on long-dated Japanese government bonds seen earlier this year has been both exceptional and unprecedented. As can be seen in the chart below, the yield on the 20-year government bond soared from around 1.9% in January to a temporary high of 2.588% in May, and meanwhile the 30-year spiked from 2.3% to 3.18%. Astonishingly, this represents the highest level seen so far since the start of 30-year issuance back in September 1999 and symbolizes more than any other single data point that Japan has entered a new macroeconomic reality.

What caused these seismic movements?

Our view is that three factors combined to create the conditions necessary to drive yields to such historic levels, namely:

- Higher-than-expected Japanese inflation numbers, especially in terms of rice and other staple food items

- The start of a rate hiking cycle by the Bank of Japan and in general a move away from loose monetary policy

- Concerns over the deteriorating fiscal position and the long-term sustainability of Japan’s national debt.

These macroeconomic factors provided the backdrop to the recent bout of selling which pushed yields up to new highs. Furthermore, the elevated selling activity was coupled with a contraction in demand which served to amplify the effect on price.

The BoJ has left the building

It’s important for international observers to remember that for Japanese government bonds with maturities over 10 years, the Bank of Japan (BoJ) has always been by far the largest single buyer. As such, the comparatively sudden reversal of the loose monetary policy which had been in place for decades represented a severe shock to the market.

At the end of 2024, the BoJ held approximately 560 trillion yen of Japanese government bonds. This accounted for nearly half of the total outstanding issuance, giving the BoJ extraordinary influence in both the primary and the secondary markets. However, the outsized role of the central bank is nowhere more pronounced than at the long-end of the curve where other buyers are few and far between. The higher duration risk and lower liquidity of these long-dated instruments tend to make them less appealing to other market participants. This means that when the BoJ reduces its buying activity there are simply no other buyers ready or able to take up the slack and prices fall.

Evolution in the symbiotic relationship between Japan’s central bank and government

As we have seen, during the recent turmoil some points on the yield curve reached thoroughly abnormal levels. Typical examples are the yields for 10-year and 20-year forwards, with the hypothetical 10-year rate starting 10 years from now (known as "10Y10Y") which exceeds 3%, and the "20Y10Y" even reaching 4%.

Although these numbers might sound modest to an international audience, it’s worth bearing in mind that since 1994 Japan's core CPI has generally remained below 1%. To find core CPI exceeding 3%, we need to delve all the way back to January 1985 when a reading of +3.2% was recorded and the Japanese economy grew by 5.1% in real terms and by 7.5% in nominal term.

This context underlines the extreme abnormality of the values recently achieved for the 10-year government bond yield projected 10 and 20 years forward. These data-points are now directly impacting primary issuance decisions via a peculiar feedback loop possible due to the sheer level of market concentration. With the Japanese Ministry of Finance last month announcing that they intend to scale back their issuance of ultra-long-term bonds, supply is already pre-emptively responding to an assumed lack of future demand for such long-dated securities.

This ongoing feedback loop actually ran further than this though, with the BoJ then subsequently agreeing to slow the pace of its reduction in government bond purchases to forestall any repeat of the recent spikes in yields.

Indeed, the central bank has now publicly committed to slowing its drop-off in purchases from a planned reduction of "400 billion yen per quarter" to a more modest "200 billion yen per quarter" starting in April 2026. The fact that this tapering is not due to commence at all until Q2 2026 signals that the BoJ understands just how structurally significant they are to the market for Japanese government debt.

What’s coming next?

Regardless of whether the BoJ implements additional rate hikes, the currently high long-term interest rates and the steepening yield curve are likely to continue to be affected by the ongoing interactions between the BoJ and the Ministry of Finance.

What is certain is that the forces moving prices in the market for Japanese government debt are now both less range-bound and less predictable than they have been for several decades, and therefore a wider range of yields are likely to be realized across the curve from now on.

Invest with us

If you have any account or dealing enquiries, please contact BBH using the following contact details:

Brown Brothers Harriman (Luxembourg) S.C.A.

80, route d’Esch, L-1470 Luxembourg

T: +352 474 066 226

F: +352 474 066 401

E: Lux.BBH.Transfer.Agent@BBH.com

Richard HAXE

Managing Director, Head of Business Development

Alex BARRY

Executive Director, Head of Distribution - UK and Ireland

Chloé CHOQUIN

Director, Business Development & Client Relations

Thomas CARTWRIGHT

Director, Business Development & Client Relations

|

Disclaimer An investment’s value and the income deriving from it may fall, as well as rise, due to market and currency fluctuations. Investors may not get back the amount originally invested. The information on this website is not intended to be investment advice, tax, financial or any other type of advice, and is for general information purposes only without regard to any particular user's investment objectives or financial situation. The information is educational only and should not be construed as an offer, solicitation, or recommendation to buy, sell, or transact in any security including, but not limited to, shares in any fund, or pursue any particular investment strategy. Any forecasts, figures, opinions or investment techniques and strategies set out are for information purposes only, and are based on certain assumptions and current market conditions that are subject to change without prior notice. The views of Sumitomo Mitsui DS Asset Management (UK) Limited reflected may change without notice. In addition, Sumitomo Mitsui DS Asset Management (UK) Limited may issue information or other reports that are inconsistent with, and reach different conclusions from, the information presented in this report and is under no obligation to ensure that such other reports are brought to the attention of any recipient of this report. Decisions to invest in any fund are deemed to be made solely on the basis of the information contained in the prospectus and the PRIIPS KID accompanied by the latest available annual and semi-annual report. |