| Capital at risk. All investments involve risk and investors may not get back the amount originally invested. |

The response both domestically and around the world to the announcement that Sanae Takaichi had triumphed in the race to replace Prime Minister Shigeru Ishiba was unanimous. Takaichi is seen as a leader of strong convictions and her steadfast support for the expansionary fiscal agenda had boosted the stock market and US dollar/Yen rate significantly just after the election.

However, we believe that Takaichi’s policies and approach should be broadly positive for the Japanese economy, we harbour some doubts over just how difficult she will likely find it to put her ideas into action. Given that her party does not currently hold a majority in the upper and lower houses, and that some influential figures in her party are opposed to her expansionary view of fiscal policy, we still need to be convinced over how far and how fast her reform agenda can move. In particular, considering the need to accommodate coalition partners and factions within the party, it seems doubtful that she can openly pursue a pro-U.S. and anti-China stance.

In this Chart of the Month, we zero in on what has been happening with valuations in the Japanese market, and therefore what sort of starting point the markets were at when they reacted so positively to the news of Takaichi’s victory.

Beneath the placid surface, things are changing at the Bank of Japan

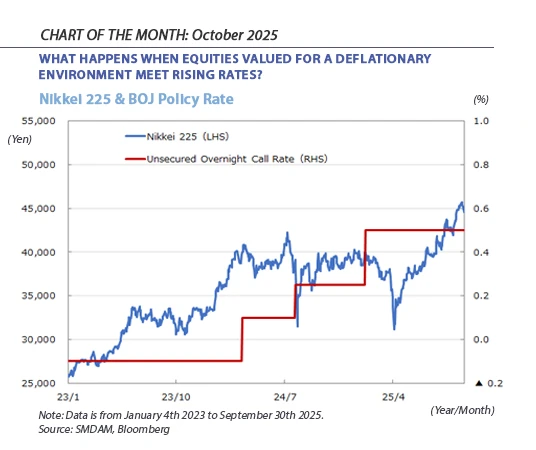

The Bank of Japan’s (BoJ) September policy meeting delivered no change to interest rates. Whilst this result was widely expected, the meeting itself was anything but routine. Two board members, Mr. Takata and Mr. Tamura, broke ranks by voting against holding rates steady and called for rates to rise to push ahead with the normalization project. More striking still, the BoJ announced it would begin selling the extensive Japanese equity ETF and REIT holdings it had accumulated during years of ultra-loose policy.

ETF purchases were once a symbol of the central banks determination to banish deflation once and for all. By providing, in effect, a ‘buyer-of-last-resort’ for certain assets, the BoJ acted to support valuations and provide liquidity to the trading system. The soon to commence unwinding of these substantial holdings signals a clear intent to continue to normalize monetary policy. Market participants have not missed this message and the direction of travel that it implies, and traders promptly priced in earlier rate hikes.

‘Normal’ for who?

Monetary normalization is undoubtedly welcome for the economy, for so long held back by persistent deflation and the distorted incentives this pushed onto firms and consumers. For equities, however, normalization it is less benign. Higher policy rates lift the entire yield curve, tightening financial conditions and raising the return investors demand from stocks. That pushes up earnings yields while also exerting downward pressure on share prices.

History offers little comfort. As can be seen in the chart below, in the past two years every BoJ rate hike has triggered an equity pullback. Zero rates back in the days of entrenched deflation meant stocks were effectively existing in zero gravity: once they moved for any exogenous reason, markets could simply drift higher on momentum alone. In a world where financial gravity — interest rates — reasserts itself, constant thrust is needed to keep market momentum going. This is in the long-run no bad thing, and as can be seen in the same chart, each rate hike induced pullback was subsequently followed by a market rise to a higher level than had held previously. However, the conditions required for the market to continue to progress upwards become incrementally more arduous after each rate rise.

Higher for longer? Rates, markets, or both?

Japan is for many global investors the epitome of a value market. Japanese equities have surged on the back of former internal affairs minister Sanae Takaichi’s triumph in the leadership race of the ruling Liberal Democratic Party. Can Japanese equities withstand the next rate hike? History, and common sense, suggests caution. “This time is different” may be too bold a bet. However, despite the market’s strong run over the past few years, Japanese equities still remain attractively valued in comparison to some other developed markets. Overall, we expect the ongoing monetary normalisation to be beneficial for Japan, but how the new administration handles this in the years ahead will be crucial.

Risk warning: The figures refer to the past and that past performance is not a reliable indicator of future results. Performance is shown in JPY, the return may increase or decrease as a result of currency fluctuations.

Invest with us

If you have any account or dealing enquiries, please contact BBH using the following contact details:

Brown Brothers Harriman (Luxembourg) S.C.A.

80, route d’Esch, L-1470 Luxembourg

T: +352 474 066 226

F: +352 474 066 401

E: Lux.BBH.Transfer.Agent@BBH.com

Richard HAXE

Managing Director, Head of Business Development

Alex BARRY

Executive Director, Head of Distribution - UK and Ireland

Chloé CHOQUIN

Director, Business Development & Client Relations

Thomas CARTWRIGHT

Director, Business Development & Client Relations

|

Disclaimer An investment’s value and the income deriving from it may fall, as well as rise, due to market and currency fluctuations. Investors may not get back the amount originally invested. The information on this website is not intended to be investment advice, tax, financial or any other type of advice, and is for general information purposes only without regard to any particular user's investment objectives or financial situation. The information is educational only and should not be construed as an offer, solicitation, or recommendation to buy, sell, or transact in any security including, but not limited to, shares in any fund, or pursue any particular investment strategy. Any forecasts, figures, opinions or investment techniques and strategies set out are for information purposes only, and are based on certain assumptions and current market conditions that are subject to change without prior notice. The views of Sumitomo Mitsui DS Asset Management (UK) Limited reflected may change without notice. In addition, Sumitomo Mitsui DS Asset Management (UK) Limited may issue information or other reports that are inconsistent with, and reach different conclusions from, the information presented in this report and is under no obligation to ensure that such other reports are brought to the attention of any recipient of this report. Decisions to invest in any fund are deemed to be made solely on the basis of the information contained in the prospectus and the PRIIPS KID accompanied by the latest available annual and semi-annual report. |