| Capital at risk. All investments involve risk and investors may not get back the amount originally invested. |

Insight

How does SMDAM interpret the recent uptick in Japanese inflation? Our Chief Global Strategist, Hisashi Shiraki takes a look at the CPI data and analyses what this means for the Japanese economy.

"In 2024, significant changes in political leadership happened globally. In the US, the presidency had shifted from Democrat Joe Biden to Republican Donald J. Trump. In the UK, the government changed for the first time in 14 years, with the Labor Party under Keir Starmer coming into power. In Germany, Chancellor Olaf Scholz faced a devastating defeat in a confidence vote, leading to the dissolution of parliament and his resignation. In France, the ruling coalition supporting President Emmanuel Macron suffered a major defeat in the parliamentary elections. Additionally, in India, the ruling coalition had struggled unexpectedly in the general elections, barely maintaining a majority but significantly losing seats. Similarly, in Japan, the ruling party, the coalition of LDP and Komeito, had experienced a historic defeat in the general elections, losing their parliamentary majority.

The widespread regime changes around the globe can be attributed to public discontent over rapid inflation following the COVID-19 pandemic. Japan, which had long struggled with deflationary pressures, has already caught up with its global peers in terms of inflation.

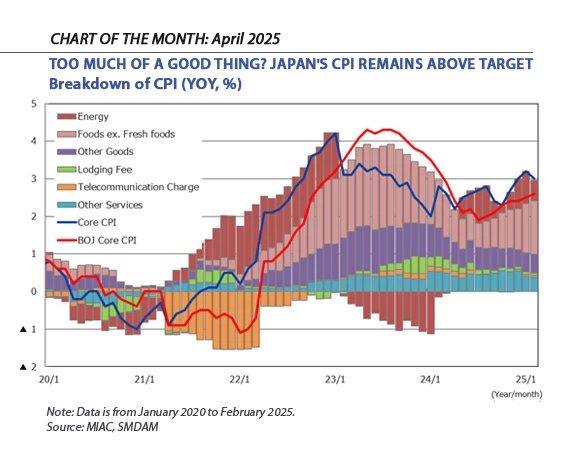

Japan, long plagued by deflation, has seen a significant change in recent years. Since April 2022, Japan’s Consumer Price Index has beaten the Bank of Japan's inflation target of 2% for 35 consecutive months.

This inflation, coupled with relatively slow wage growth, has led to widespread dissatisfaction directed at the ruling party and Prime Minister Ishiba. The rising food prices have further fueled public anger. In February 2025, the CPI increased by 3.66% YOY, with 2.16% of this increase attributed to food prices, which make up only about 26% of the CPI's weight.

Among food prices, the surge in rice prices, a staple food for Japanese people, has been particularly severe. The CPI for rice in February rose by 80% year-on-year, marking the highest increase on record. Due to prolonged deflation and low economic growth, Japan's Engel coefficient has been rising, meaning the actual perceived inflation rate, especially among low-income households, far exceeds the official CPI rate of 3.66%. According to the Bank of Japan's "Survey on Household Finances," consumers feel that prices have risen by approximately 15% year-on-year.

While the positive cycle of price increases and inflation is steering the Japanese economy towards normalization, public dissatisfaction is aligning with that of people in other countries. This summer, Japan is scheduled to hold its triennial House of Councillors election. Given the ruling party and Prime Minister Ishiba's failure to effectively address the persistent inflation, their chances of victory appear slim. The bull market in the Japanese stock market began with the return of the LDP as the ruling party with the election of PM Abe in December 2012. If the ruling LDP lose power after the election in the summer, it could significantly impact the stock market subsequently."

Invest with us

If you have any account or dealing enquiries, please contact BBH using the following contact details:

Brown Brothers Harriman (Luxembourg) S.C.A.

80, route d’Esch, L-1470 Luxembourg

T: +352 474 066 226

F: +352 474 066 401

E: Lux.BBH.Transfer.Agent@BBH.com

Richard HAXE

Managing Director, Head of Business Development

Alex BARRY

Executive Director, Head of Distribution - UK and Ireland

Chloé CHOQUIN

Director, Business Development & Client Relations

Thomas CARTWRIGHT

Director, Business Development & Client Relations

|

Disclaimer An investment’s value and the income deriving from it may fall, as well as rise, due to market and currency fluctuations. Investors may not get back the amount originally invested. The information on this website is not intended to be investment advice, tax, financial or any other type of advice, and is for general information purposes only without regard to any particular user's investment objectives or financial situation. The information is educational only and should not be construed as an offer, solicitation, or recommendation to buy, sell, or transact in any security including, but not limited to, shares in any fund, or pursue any particular investment strategy. Any forecasts, figures, opinions or investment techniques and strategies set out are for information purposes only, and are based on certain assumptions and current market conditions that are subject to change without prior notice. The views of Sumitomo Mitsui DS Asset Management (UK) Limited reflected may change without notice. In addition, Sumitomo Mitsui DS Asset Management (UK) Limited may issue information or other reports that are inconsistent with, and reach different conclusions from, the information presented in this report and is under no obligation to ensure that such other reports are brought to the attention of any recipient of this report. Decisions to invest in any fund are deemed to be made solely on the basis of the information contained in the prospectus and the PRIIPS KID accompanied by the latest available annual and semi-annual report. |