| Capital at risk. All investments involve risk and investors may not get back the amount originally invested. |

Highlights:

|

Contextualizing the caution

The title of this article refers to a well-known Japanese proverb. Whilst stone bridges are generally a highly reliable method of crossing a river, it’s not impossible that it will collapse upon taking the extra weight of the latest traveler. Hence, the cautious character being gently mocked in the saying is exhibiting undue or excessive caution by tapping the bridge to check it doesn’t fall down.

We believe Japanese corporates are guilty of metaphorically ‘taping the stone bridge’, as it were, with their latest FY2025 forecasts. As we will outline in this article, the robust performance seen in 2024 mean that corporate Japan enters today’s much more uncertain setting from a position of stability and strength. The caution generally displayed in these forecasts is, however, completely understandable when taking into account the market turmoil unleashed by President Trump’s ‘Liberation Day,’ and the subsequent shifts in the U.S.’s policy. As such, we have attempted to categorize the various approaches forecasters have taken to this issue below.

FY2024 summary

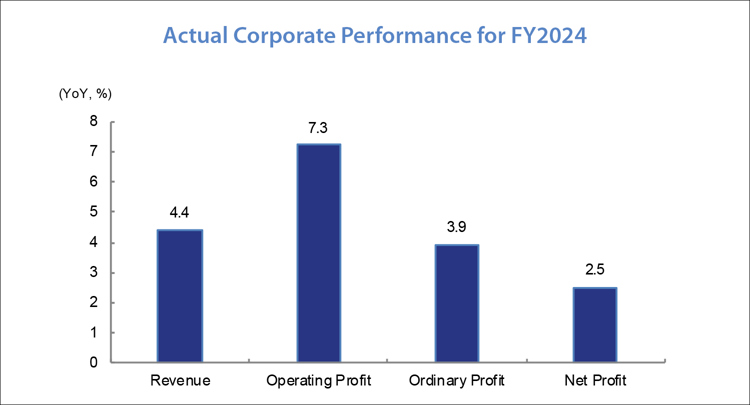

Many Japanese companies have fiscal years ending in March. As such, each year April provides a slew of FY results which taken in aggregate offer a clear overview of the Japanese corporate landscape. The headline so far according to SMDAM’s Japan Equity research team is that Japanese corporate performance was healthy if short of spectacular in 2024. Importantly, this solid corporate performance registered for FY2024 suggests the economy entered the current period of uncertainty on a reasonably strong footing. This is part of why we see the cautious approach taken in many of these forecasts as slightly excessive.

As of May 16, over 99% of TOPIX ex-financial companies with fiscal years ending in March have completed their FY2024 earnings announcements. As can be seen in the graph below, the results showed single-digit year-on-year growth, with revenue increasing by 4.4%, operating profit by 7.3%, ordinary profit by 3.9%, and net profit by 2.5%.

2025 has seen global economic uncertainty intensify due to the trade policies implemented by the Trump administration. As a result, investors are placing high emphasis on companies’ own forecasts for FY2025 to see what impacts they are anticipating. SMDAM’s Japanese Equity research team has been focused on analysing these forecasts and we summarize our key findings below.

The road ahead – what do we expect for 2025?

As we have seen, Japanese corporate performance held up well in 2024. However, the macroeconomic and geopolitical uncertainty unleashed in Q1 2025 are expected to lead to modest declines in both revenue and profit for FY2025. However, given the lack of clarity around U.S. tariff policy today, things could rapidly improve if a less antagonistic trade relationship starts to crystallize.

Our view at SMDAM is that there have been three main approaches to factoring the trade uncertainty into FY2025 forecasts. Companies analysed by SMDAM have either:

• Assumed tariffs will be implemented at the elevated levels currently proposed and will therefore have a clearly negative impact on earnings;

• Assumed tariffs may happen, but that their extent and level will likely be limited by negotiations, and therefore the impact will less severe than in the worst-case scenario above; or

• Acknowledged the high level of uncertainty around trade policy by refraining from publishing a forecast at this stage.

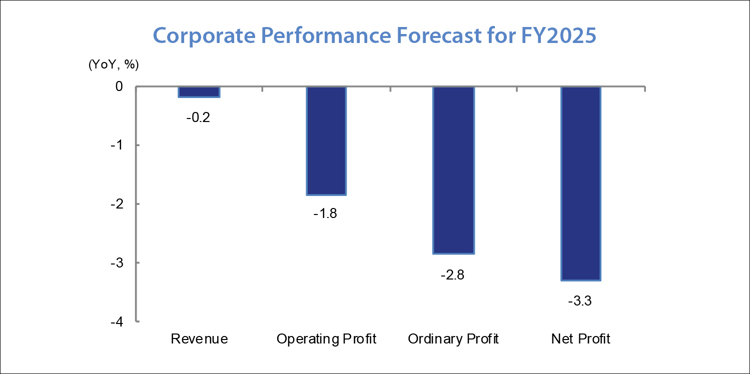

According to the results of our research, Japanese companies’ own forecasts for FY2025 indicate an expected year-on-year decrease in revenue by -0.2%, operating profit by -1.8%, ordinary profit by -2.8%, and net profit by -3.3%.

Observers in Japan and around the world have seen how the Trump administration’s tariff policies can change very suddenly. This makes it difficult to assess the probability that what is announced at one time will actually be implemented. As such, it is understandable that a range of different responses have been produced along the lines described above, and that many forecasts have tended on the cautious side.

Reasons to be cheerful

The market had already anticipated the subdued forecasts that emerged over April. Moreover, since the forecasts have generally favored mild pessimism, there is significant potential for stock price appreciation to take place if there is progress on tariff issues.

Another layer of complexity is added by movements in the exchange rate. The prospect for continued strengthening of the yen relative to other major global currencies needs to be taken into account. Shortly before earnings announcements began in late April, on April 1 the Bank of Japan published the March results of the nationwide Short-term Economic Survey of Enterprises (Tankan).

According to this widely watched survey, exporting companies and large manufacturers are assuming an average exchange rate of 147.35 yen per dollar and 158.05 yen per euro for their FY2025 business plans. Since fluctuations in the yen exchange rate can be a factor for revising performance forecasts, it is important to consider these levels as a reference moving forwards.

Conclusions

Our view at SMDAM is that the market had anticipated the modest forecasts recently put forward by Japanese corporates. Therefore, we are unlikely to see increased selling activity driven by these. Additionally, since the initial forecasts have been conservative, if there were to be a clear trend towards a reduction global trade tension, there is significant potential for the market to rebound strongly. If upward revisions to the cautious FY2025 forecasts were to emerge, this would create a strong narrative of Japanese corporate resilience.

We understand why the forecasters have seen fit to ‘tap the stone bridge’ and display caution; we also remain optimistic that underneath the noise, the strong fundamental case for Japanese equities remains intact.

Invest with us

If you have any account or dealing enquiries, please contact BBH using the following contact details:

Brown Brothers Harriman (Luxembourg) S.C.A.

80, route d’Esch, L-1470 Luxembourg

T: +352 474 066 226

F: +352 474 066 401

E: Lux.BBH.Transfer.Agent@BBH.com

Richard HAXE

Managing Director, Head of Business Development

Alex BARRY

Executive Director, Head of Distribution - UK and Ireland

Chloé CHOQUIN

Director, Business Development & Client Relations

Thomas CARTWRIGHT

Director, Business Development & Client Relations

|

Disclaimer An investment’s value and the income deriving from it may fall, as well as rise, due to market and currency fluctuations. Investors may not get back the amount originally invested. The information on this website is not intended to be investment advice, tax, financial or any other type of advice, and is for general information purposes only without regard to any particular user's investment objectives or financial situation. The information is educational only and should not be construed as an offer, solicitation, or recommendation to buy, sell, or transact in any security including, but not limited to, shares in any fund, or pursue any particular investment strategy. Any forecasts, figures, opinions or investment techniques and strategies set out are for information purposes only, and are based on certain assumptions and current market conditions that are subject to change without prior notice. The views of Sumitomo Mitsui DS Asset Management (UK) Limited reflected may change without notice. In addition, Sumitomo Mitsui DS Asset Management (UK) Limited may issue information or other reports that are inconsistent with, and reach different conclusions from, the information presented in this report and is under no obligation to ensure that such other reports are brought to the attention of any recipient of this report. Decisions to invest in any fund are deemed to be made solely on the basis of the information contained in the prospectus and the PRIIPS KID accompanied by the latest available annual and semi-annual report. |