| Capital at risk. All investments involve risk and investors may not get back the amount originally invested. |

More than 50 years have passed since economist E.F. Schumacher published his landmark study into the virtues of small-scale economic organizations relative to their lumbering, slow-moving larger competitors. However, the insights of the classic text ‘Small is Beautiful’ remain pertinent today and still resonate with us here at Sumitomo Mitsui DS Asset Management (SMDAM), where we have always been resolute champions of the small cap space where the adaptability, innovation and pioneering spirit celebrated by Schumacher is so evident.

There is a well-known and globally esteemed pantheon of Japanese companies we are all familiar with. The Hitachis, Toyotas, and Sonys of this world are known for exemplifying excellence and displaying global leadership in their respective industries. Of the nearly 4,000 companies listed on the Tokyo Stock Exchange, these are the ones with which we are all intimately familiar already.

However, a far richer, deeper set of opportunities for future growth can be found if you look further down the market cap spectrum. With around 3,300 individual companies (or 87% of the listed names) being defined as small cap, there is a vast universe of lesser-known corporates where the global champions of tomorrow may be emerging. For the purposes of this article, we’d like to look not just at small and mid-sized companies but specifically at those trading at relatively low valuations.

Value, but not as you’ve seen it before

At SMDAM, we think that a value-focused approach works particularly well in the small cap market but our strategy isn’t a ‘typical’ value approach. On the face of it, the argument for small cap versus large over time is relatively clear. Smaller companies tend to be the originators of new ideas, lead in the development of innovative technologies, and have demonstrated faster revenue growth consistently for the past 20+ years.

Moreover, down at the small cap end of the index, the strongest performance has tended to come from value names. Small-cap investing is often associated with companies in their infancy. Whilst it is true that Japan has a very vibrant IPO market – with between 80 and 140 new listings per year in the past decade – we believe there is a more promising investment case for companies that are better established, mature, dare we say even at risk of being underappreciated.

Taking the road less travelled

To find these underappreciated but undeniably valuable companies, our team is focused on locating something subtler – the internal catalysts for change that can transform a company’s fortunes and surprise the market. This is where our local knowledge and insights becomes crucial.

We believe creating alpha from Japanese small caps comes from identifying companies where management is starting to recognise capital inefficiencies and is genuinely open to change. We want to find those companies eager to turnaround their fortunes through adopting new technologies for example, or by streamlining operations such as looking at improving inventory turnover. Perhaps they’re open to making bold capital allocation decisions like refocusing the business portfolio away from declining legacy areas and towards growth prospects.

However, crucially this isn’t just about chasing the latest growth story. It’s about investing in solid businesses where internal transformation is possible, often before this possibility has become visible to the broader market. Our team seeks to identify opportunities whose very existence will surprise the market, therefore creating the possibility for outperformance.

Beyond focusing on sector dynamics or more widely explored investment theses, we tend to look for stock-specific opportunities. A key, underappreciated aspect to investing in Japan is the need to thoroughly investigate and understand corporate and management behaviour at the individual company level. As we’ve alluded to, not all leadership teams are ready to embrace change or pursue shareholder returns. Alongside our research we seek to engage with c-suite leaders, always seeking to ask the right questions to gauge management’s appetite for self-improvement. We look for leaders with ambition and the willingness to break from tradition – not just to survive but to thrive.

What do we look for in leadership teams?

A series of factors are now aligned to create ideal conditions for Japanese corporates as a whole to thrive. This began with the Tokyo Stock Exchanges push for corporate governance reforms, but has now been augmented by increased investor pressure around the cost of capital, a new economic reality of above-zero inflation and rising interest rates, as well as the fact that a fresh generation of leaders are taking the reins of corporate Japan. Today, Japan is becoming a fertile ground for the transformation stories we hunt for.

We look for companies with open-minded, forward-looking, ambitious leaders. We then invest in them at an early stage in the hope of achieving an excess return over time as this change agenda plays out. We see the intimate knowledge we build up of the companies we research and eventually invest in as our best line of defence against so-called ‘value traps’.

We try to avoid companies where management is complacent. We sidestep those unwilling to overhaul the problematic areas in their business to improve its prospects at a fundamental level or return cash to shareholders. Conversely, we proactively engage in dialogue with companies aimed at improving medium to long-term corporate value. The key point is that even mature or declining companies can deliver excess returns if they outperform market expectations – a phenomenon more likely among small caps given their limited analyst coverage.

We look for value where others can’t

We are confident that how we define value gives us a point of difference versus many typical value-focused strategies. We don’t look for companies that are just cheap versus history, versus their peers, or versus free cash flow, for instance. We are interested in companies that are cheap compared with their own internal potential return on equity (ROE), for which we have developed a proprietary model. Not only does our team look at things from a different perspective than many of our peers; we also dive into parts of the market that are vastly under-researched.

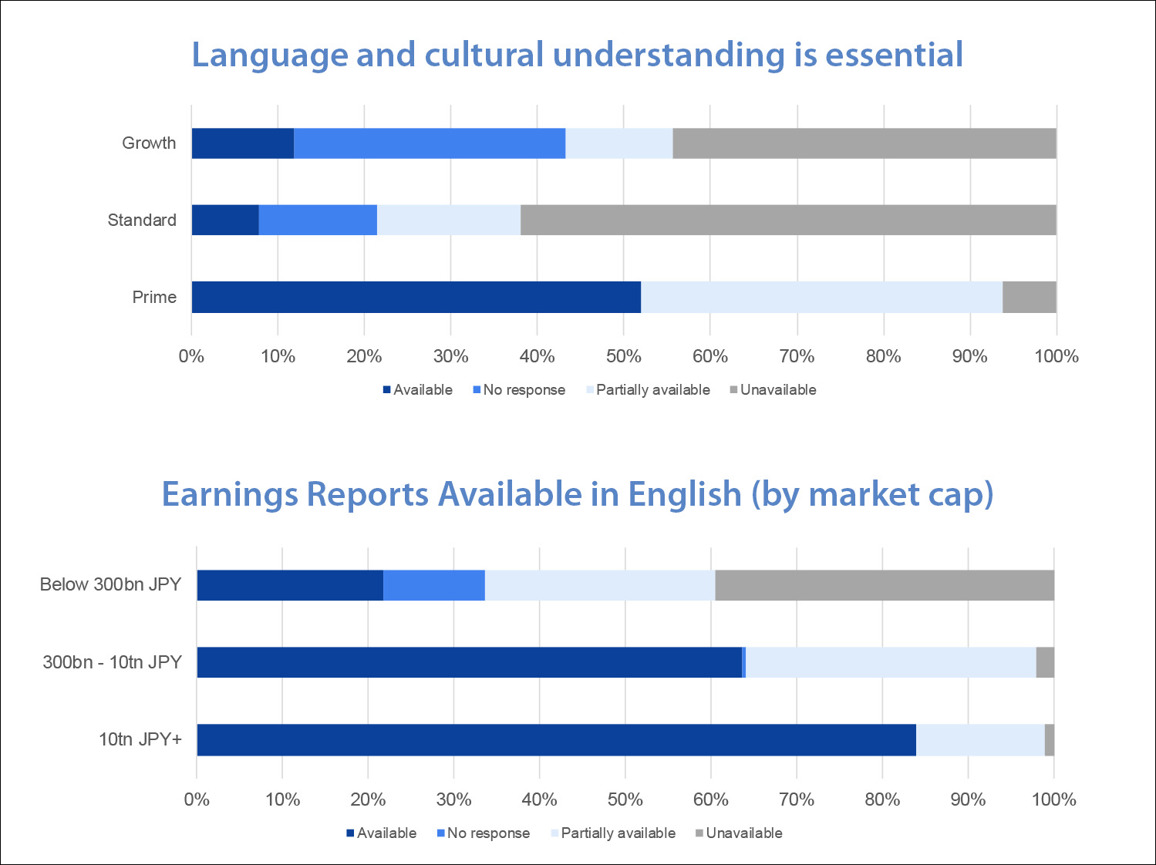

In Japanese large caps, we know an average of 16 analysts tend to cover one company, which is lower than other comparable developed markets. This number drops off significantly for mid-caps, and for small caps we are often talking about a single analyst only. This lack of coverage – and more specifically, lack of English-language coverage – is a key benefit to being based on the ground in Japan, having a team of native Japanese and fluent speaking analysts.

As can be seen from the chart below, the smaller the company, the less likely it is going to be to produce English disclosure. It’s not that they don’t want to; many of these small businesses simply don’t have the resources to publish such information.

We look for value where others can’t

With many of the headwinds facing global developed equity markets today – geopolitical tension, inflation, and currency risk – we would argue there is a case for sheltering against some of these pressures in more domestically focused companies.

In bringing in some exposure to companies more exposed to the idiosyncratic factors impacting the Japanese domestic economy, it also presents a less correlated risk/return profile for investors with a suitable tolerance and set of objectives.

Invest with us

If you have any account or dealing enquiries, please contact BBH using the following contact details:

Brown Brothers Harriman (Luxembourg) S.C.A.

80, route d’Esch, L-1470 Luxembourg

T: +352 474 066 226

F: +352 474 066 401

E: Lux.BBH.Transfer.Agent@BBH.com

Richard HAXE

Managing Director, Head of Business Development

Alex BARRY

Executive Director, Head of Distribution - UK and Ireland

Chloé CHOQUIN

Director, Business Development & Client Relations

Thomas CARTWRIGHT

Director, Business Development & Client Relations

|

Disclaimer An investment’s value and the income deriving from it may fall, as well as rise, due to market and currency fluctuations. Investors may not get back the amount originally invested. The information on this website is not intended to be investment advice, tax, financial or any other type of advice, and is for general information purposes only without regard to any particular user's investment objectives or financial situation. The information is educational only and should not be construed as an offer, solicitation, or recommendation to buy, sell, or transact in any security including, but not limited to, shares in any fund, or pursue any particular investment strategy. Any forecasts, figures, opinions or investment techniques and strategies set out are for information purposes only, and are based on certain assumptions and current market conditions that are subject to change without prior notice. The views of Sumitomo Mitsui DS Asset Management (UK) Limited reflected may change without notice. In addition, Sumitomo Mitsui DS Asset Management (UK) Limited may issue information or other reports that are inconsistent with, and reach different conclusions from, the information presented in this report and is under no obligation to ensure that such other reports are brought to the attention of any recipient of this report. Decisions to invest in any fund are deemed to be made solely on the basis of the information contained in the prospectus and the PRIIPS KID accompanied by the latest available annual and semi-annual report. |