| Capital at risk. All investments involve risk and investors may not get back the amount originally invested. |

“If you only read the books that everyone else is reading, you can only think what everyone else is thinking.”

― Haruki Murakami, Norwegian Wood

One of Japan’s most popular novelists, Murakami’s idea that imbibing the same information as everyone else will ultimately lead to the same unoriginal and repetitive thoughts resonates strongly with us here at Sumitomo Mitsui DS Asset Management (SMDAM). We celebrate unconstrained, original thinking and the new information that can encourage and facilitate this.

Nowhere is this approach more essential than in the small-cap space, where highly idiosyncratic and company-specific factors are always in play. Without the detailed due diligence and often face-to-face contact with company management, it simply isn’t possible to see through the noise to the true value of a stock. In short, the best small-cap managers aren’t afraid to ‘read the books no-one else is reading,’ and sometimes to think the thoughts that no one else is thinking.

Small-cap companies and how to successfully navigate through the vast universe of available stocks was the topic addressed by Alex Hart from SMDAM, Olivia Micklem from Artemis, and George Cooke from Montanaro at SMDAM’s latest multi-manager investment symposium. While each presentation had a different regional focus – from the US to Japan and Europe ex-UK – the common theme of the event was that allocators who have avoided the small-cap space due to fear of the long-anticipated but still absent recession have missed out on some great returns. Moreover, today there are good reasons to think remaining underweight will see further potential positive returns slip away too.

This article covers the key points made and highlights why the opportunity in small-caps today may be too big to ignore.

True diversification means more than just going ‘global’

All three speakers agreed that developed market small-caps in general have massive untapped potential as diversifiers today. With allocators increasingly aware that so-called ‘global’ strategies are often less diversified than expected, the need to access returns less correlated to US indices has become apparent.

A key reason small- and mid-cap stocks can display this attractive characteristic is that smaller capitalization companies are often much more reliant on domestic markets for sources of revenue than their larger counterparts. This means smaller companies are less exposed to sudden changes in the tempo of global markets, potentially providing an added layer of stability to their earnings versus large- and mega-cap stocks with global risk profiles.

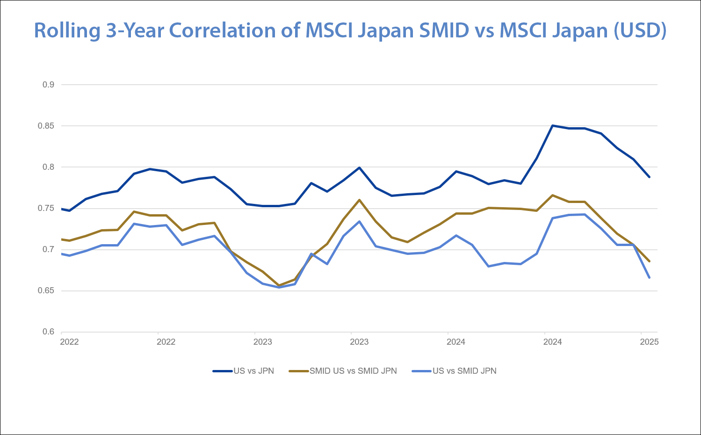

In the case of Japan as shown in the chart below, a range of rolling 3-year correlations between the US and Japan have actually been falling markedly over the past 12 months. As such, the small- and mid-cap space can provide a source of less correlated returns to investors eager to hedge their exposure to the US market in general.

Risk warning: Past performance is not a reliable indicator of future performance and may not be repeated. An investment’s value and the income deriving from it may fall, as well as rise, due to market fluctuations. Investors may not get back the amount originally invested. Performance is shown in USD, the return may increase or decrease as a result of currency fluctuations, and is gross of fees (after trading expenses).

High dispersion means you need to be active

Any small-cap manager must have a satisfactory answer to the question as to how they avoid value traps, and all three contributors to our symposium sought to address this question in some manner. A common theme that emerged across all presentations was that a disciplined and repeatable investment process was vital for accomplishing this.

As Alex Hart emphasized, it is not enough for a company to be simply undervalued – there are many undervalued companies out there, a large amount of which will either never realize their intrinsic value or will take in inordinate amount of time to do so. The magic combination a small-cap value-focused manager needs to uncover is an undervalued company with a plausible pathway to achieve consistently higher levels of return on equity through internally driven corporate change. And this is, of course, easier said than done!

In the case of Japan, the narrative around improving corporate governance as a catalyst for the market is by now quite well known. In practice, this means finding names where management are showing a real, tangible desire to embrace change.

Alex ran through an example underlining the specific signals identified that showed this willingness to change. The story was told from the company’s initial incorporation in 2015, through a complex merger in 2020, followed by a re-brand and re-structure in 2022 to show just how closely you have to look to truly understand a company’s value-proposition and how this is

evolving over time.

The high dispersion of returns seen in the long tail of small-cap companies means finding the winners is rarely a straightforward problem, and Alex urged that investors should be willing to hold their managers to account over their ability or inability to explain precisely when and why they are entering or exiting positions.

The “barbarians” are at the gates – do they know

something you don’t?

Another repeating motif from the event was that the high quality of the small-cap sectors of many developed markets has been underlined over recent years by the sheer volume of private equity activity. Whilst this might sound paradoxical, the fact that some of the most sophisticated private equity investors in the world see the valuations on offer in the listed small-cap space as so attractive reminds us that smaller companies are not lacking suitors today.

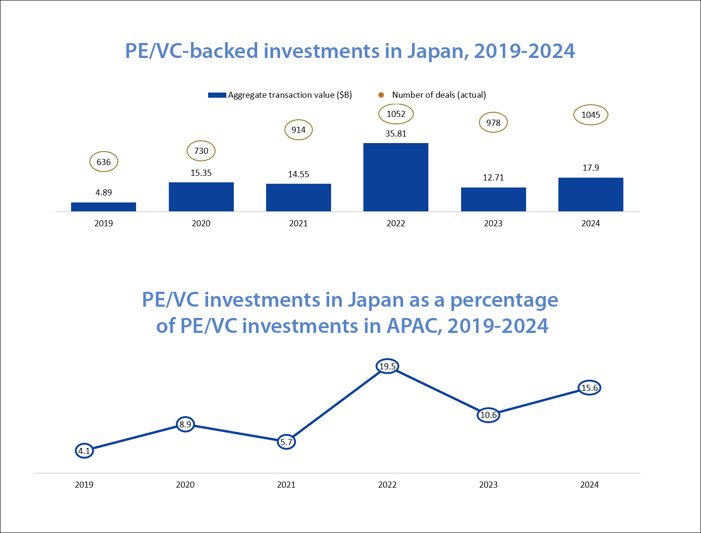

As the graphic below shows, private capital has now firmly discovered Japan, and listed companies accordingly have another set of market participants they must adapt in response to.

Data compiled Jan. 17, 2025. PE/VC = private equity orventure capital.

Analysis includes global whole-company acquisitions, minority stake acquisitions, and asset acquisitions, and rounds of funding announced between Jan. 1, 2019, and Dec. 31, 2024, where the buyer/investor in the deal is or includes a private equity or venture capital firm, and where the transaction geography is in Japan or Asia-Pacific. Excludes terminated deals and add-on acquisitions.

In one sense, this can be interpreted as an endorsement of the quality of many listed companies and the attractiveness of the valuations on offer. Additionally, the increasing presence of the “barbarians at the gate,” as the 1988 non-fiction classic about the leveraged buyout of RJR Nabisco so memorably called them, also provides several additional drivers of performance that public-market investors can potentially benefit from.

Notably, the increased presence in the market of private equity can have a similar impact to traditional activist investors and may compel listed company management teams to focus more on shareholder value. This could manifest through efforts to raise the return on equity, return excess cash to shareholders, think carefully about their M&A strategy and how to execute this to maximize shareholder returns, carry out increased share

buybacks, and in general to maximize efficiency across their

business operations.

Companies that are incentivized to achieve corporate and operational excellence will keep existing shareholders happy, thus quelling calls for management or ownership changes. This will also have the benefit of meaning that if the company is taken private, a decent multiple will be likely to be applied, thus rewarding existing shareholders with an attractive premium.

In these related ways, expanded private equity activity can

potentially be seen as another catalyst to unlock value and incentivize desirable behaviours in management teams.

Are smaller companies finally due their moment

in the sun?

The following themes were recurring across all three presentations:

• Small-caps can provide a risk/return profile that favourably complements the returns on offer from large-caps, and US large caps in particular;

• Under-researched and under-valued companies provide an ideal hunting ground for active stock picking; and

• Smaller companies are looking increasingly attractive to private capital, with potentially interesting consequences for investors who may see raised performance in the meantime, and attractive premiums if M&A activity occurs within their portfolio

All three speakers implicitly agreed that searching for hidden gems in the small-cap universe means being willing and able to think the thoughts that other investors aren’t thinking, and this inevitably involves a willingness to go off the beaten path. SMDAM’s small-cap specialist portfolio management team are committed to ‘reading the books no one else is reading,’ or at the very least re-reading the books other people may have

misinterpreted, to find those undervalued, under-researched companies that we believe can unlock fantastic value for our clients.

In order to learn more about SMD-AM and our range of small-and mid-cap investment strategies, please visit our website

Invest with us

If you have any account or dealing enquiries, please contact BBH using the following contact details:

Brown Brothers Harriman (Luxembourg) S.C.A.

80, route d’Esch, L-1470 Luxembourg

T: +352 474 066 226

F: +352 474 066 401

E: Lux.BBH.Transfer.Agent@BBH.com

Richard HAXE

Managing Director, Head of Business Development

Alex BARRY

Executive Director, Head of Distribution - UK and Ireland

Chloé CHOQUIN

Director, Business Development & Client Relations

Thomas CARTWRIGHT

Director, Business Development & Client Relations

|

Disclaimer An investment’s value and the income deriving from it may fall, as well as rise, due to market and currency fluctuations. Investors may not get back the amount originally invested. The information on this website is not intended to be investment advice, tax, financial or any other type of advice, and is for general information purposes only without regard to any particular user's investment objectives or financial situation. The information is educational only and should not be construed as an offer, solicitation, or recommendation to buy, sell, or transact in any security including, but not limited to, shares in any fund, or pursue any particular investment strategy. Any forecasts, figures, opinions or investment techniques and strategies set out are for information purposes only, and are based on certain assumptions and current market conditions that are subject to change without prior notice. The views of Sumitomo Mitsui DS Asset Management (UK) Limited reflected may change without notice. In addition, Sumitomo Mitsui DS Asset Management (UK) Limited may issue information or other reports that are inconsistent with, and reach different conclusions from, the information presented in this report and is under no obligation to ensure that such other reports are brought to the attention of any recipient of this report. Decisions to invest in any fund are deemed to be made solely on the basis of the information contained in the prospectus and the PRIIPS KID accompanied by the latest available annual and semi-annual report. |