| Capital at risk. All investments involve risk and investors may not get back the amount originally invested. |

Insight

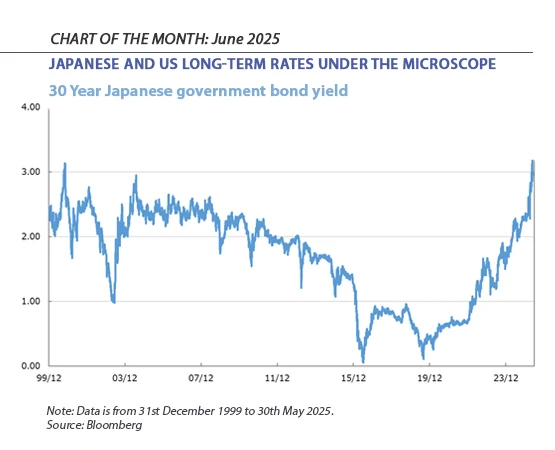

Chart of the Month for June puts the dramatic changes in the Japanese interest rate environment in context, both domestically and globally.

SMDAM’s view is that the seismic shifts taking place today need to be seen as part of a global pattern, but one that is playing out in different economies in very different ways.

As can be seen in the chart above, the yield on long-dated Japanese government bonds has recently surged to levels rarely seen before. The 30-year yield is hovering just below all-time highs, while the 40-year yield has now exceeded its previous all-time high set decades ago.

This phenomenon is not exclusive to Japan, with long-term interest rates globally displaying an upward trend. The reasons behind the various spikes in government borrowing costs, however, are often nationally specific. As such, we need to pay particular attention to local political and economic conditions to understand the causes of these shifts. In the US, for example, the primary reason for the jump in long-term rates has been concerns over the US’s long-term fiscal position caused by the Trump tax cuts.

The situation in Japan is completely different, and accordingly SMDAM’s analysis focuses on different factors.

Japan is currently in the process of monetary tightening against the backdrop of a relatively weak domestic economy. Given the negative real GDP growth in the first quarter of 2025, SMDAM’s view is that it is now unlikely we will see a rapid normalization of Japanese interest rates. We expect the Bank of Japan will proceed to cautiously raise its policy rate, with the current rate of 0.5% anticipated to reach 0.75% by April next year, followed by hitting 1% by October 2026.

So, why have Japan’s long-term interest rates surged in the context of slowing growth? Our view is that supply and demand shifts are driving this rather than fundamentals. Specifically, the Bank of Japan, which has been by far the largest buyer in the Japanese government bond market, has pivoted towards an exit from quantitative easing. This has effectively translated into a demand shock that has rapidly moved the market towards a new equilibrium price as the largest purchaser has switched gears into buying at a much lower scale.

The Bank of Japan has provided forward guidance that it plans to progressively reduce its bond purchases from around 5.7 trillion yen per month as of July last year by approximately 400 billion yen per quarter. This puts the central bank on a glide path down towards purchases of roughly 2.9 trillion yen per month by the first quarter of 2026. It is this dramatic and relatively swift reduction in the Bank of Japan's support for long-term bond prices – instruments which have limited other sources of demand able to take up the slack – which has caused the rise in market interest rates.

Therefore, the Japanese story differs fundamentally from the US story of declining fiscal credibility. This is evidenced by the fact that the 10-year real interest rate on Japanese government bonds remains negative, suggesting that there is still room for the yield curve to rise further.

On the other hand, since the sharp rise in long-term rates was driven by supply and demand rather than fundamentals, it is also possible that the longer end of the curve may actually flatten. If this flattening were to occur, it would certainly run against the grain of recent macroeconomic data, which has suggested the end of deflation, a return to mild inflation, and a continuing normalization of interest rates.

That a flattening of the long-end of the Japanese government yield curve is even a distant possibility tells us a lot about the unprecedented situation we are seeing today in government bond markets. This hypothetical possibility of the yield curve flattening is a side effect of the unprecedented monetary easing underway by the Bank of Japan. The scale and significance of this shift can hardly be overstated, and we expect to have a great deal more to say on this topic as the situation evolves and unfolds over the coming quarters.

Invest with us

If you have any account or dealing enquiries, please contact BBH using the following contact details:

Brown Brothers Harriman (Luxembourg) S.C.A.

80, route d’Esch, L-1470 Luxembourg

T: +352 474 066 226

F: +352 474 066 401

E: Lux.BBH.Transfer.Agent@BBH.com

Richard HAXE

Managing Director, Head of Business Development

Alex BARRY

Executive Director, Head of Distribution - UK and Ireland

Chloé CHOQUIN

Director, Business Development & Client Relations

Thomas CARTWRIGHT

Director, Business Development & Client Relations

|

Disclaimer An investment’s value and the income deriving from it may fall, as well as rise, due to market and currency fluctuations. Investors may not get back the amount originally invested. The information on this website is not intended to be investment advice, tax, financial or any other type of advice, and is for general information purposes only without regard to any particular user's investment objectives or financial situation. The information is educational only and should not be construed as an offer, solicitation, or recommendation to buy, sell, or transact in any security including, but not limited to, shares in any fund, or pursue any particular investment strategy. Any forecasts, figures, opinions or investment techniques and strategies set out are for information purposes only, and are based on certain assumptions and current market conditions that are subject to change without prior notice. The views of Sumitomo Mitsui DS Asset Management (UK) Limited reflected may change without notice. In addition, Sumitomo Mitsui DS Asset Management (UK) Limited may issue information or other reports that are inconsistent with, and reach different conclusions from, the information presented in this report and is under no obligation to ensure that such other reports are brought to the attention of any recipient of this report. Decisions to invest in any fund are deemed to be made solely on the basis of the information contained in the prospectus and the PRIIPS KID accompanied by the latest available annual and semi-annual report. |