| Capital at risk. All investments involve risk and investors may not get back the amount originally invested. |

Insight

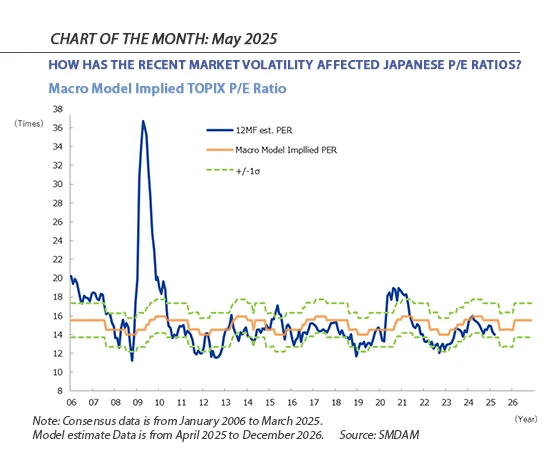

Investors were relieved that May saw reduced levels of volatility compared to April. However, significant uncertainty remains, and this means attention is naturally focused on valuation metrics such as price-earnings ratios (PER). SMDAM's research platform has been exploring how our quant model's estimated PER compares to market consensus, and what this implies about Japanese equity valuations looking ahead.

Our Chart of the Month for May 2025 shows the estimated PER of the TOPIX as produced by our proprietary quant model, plotted against the market consensus estimated 12-month forward PER.

As indicated by the orange line in the chart, our model's estimated p/e ratio for the TOPIX is projected to trend downwards into the second half of 2025.

This contraction in valuations is a result of the increasing global economic uncertainty caused by the Trump tariffs, and follows the pattern established in global markets since the correction of early April.

However, while these short-term trends look bearish, the blue line on the chart shows that the consensus PER is currently about one standard deviation below the fair value p/e ratio as suggested by our model (indicated by the orange line).

Importantly, this suggests the market is currently undervalued, and therefore the potential for further value compression is limited. The fact that during the market adjustment in April the 12-month forward p/e ratio for the TOPIX temporarily dropped below 12 times also suggests that the Japanese market has already largely corrected and the uncertainty has been priced in.

Since the summer of 2024, the PER of the TOPIX has continued to move within this undervalued rang, namely between the fair value produced by our model minus one standard deviation. This undervaluation can mainly be attributed to the impact of the Bank of Japan's (BoJ) monetary tightening. Following the recent monetary policy decision meeting, BoJ Governor Ueda remarked that "the BoJ will support the economy by the current accommodative monetary policy" amidst the global economic uncertainty due to the Trump tariffs. Our view at SMDAM is that this should be interpreted as a significant shift from the previously hawkish stance.

If the market shares our interpretation and reacts to this as we expect, the PER will probably increase. Additionally, if our view that the Japanese market has already priced in a worst-case scenario in terms of tariffs is correct, there is strong potential for upside in the Japanese market in the second half of 2025.

Risk warning: The figure refers to the past and future, past performance is not a reliable indicator of future results and forecasts are not a reliable indicator of future performance.

Invest with us

If you have any account or dealing enquiries, please contact BBH using the following contact details:

Brown Brothers Harriman (Luxembourg) S.C.A.

80, route d’Esch, L-1470 Luxembourg

T: +352 474 066 226

F: +352 474 066 401

E: Lux.BBH.Transfer.Agent@BBH.com

Richard HAXE

Managing Director, Head of Business Development

Alex BARRY

Executive Director, Head of Distribution - UK and Ireland

Chloé CHOQUIN

Director, Business Development & Client Relations

Thomas CARTWRIGHT

Director, Business Development & Client Relations

|

Disclaimer An investment’s value and the income deriving from it may fall, as well as rise, due to market and currency fluctuations. Investors may not get back the amount originally invested. The information on this website is not intended to be investment advice, tax, financial or any other type of advice, and is for general information purposes only without regard to any particular user's investment objectives or financial situation. The information is educational only and should not be construed as an offer, solicitation, or recommendation to buy, sell, or transact in any security including, but not limited to, shares in any fund, or pursue any particular investment strategy. Any forecasts, figures, opinions or investment techniques and strategies set out are for information purposes only, and are based on certain assumptions and current market conditions that are subject to change without prior notice. The views of Sumitomo Mitsui DS Asset Management (UK) Limited reflected may change without notice. In addition, Sumitomo Mitsui DS Asset Management (UK) Limited may issue information or other reports that are inconsistent with, and reach different conclusions from, the information presented in this report and is under no obligation to ensure that such other reports are brought to the attention of any recipient of this report. Decisions to invest in any fund are deemed to be made solely on the basis of the information contained in the prospectus and the PRIIPS KID accompanied by the latest available annual and semi-annual report. |