| Capital at risk. All investments involve risk and investors may not get back the amount originally invested. |

This month we focus on the strength and momentum of the Japanese stock market which has recently repeated its achievement of last June by once again pushing ahead to a new all-time high. How do we interpret this development, and what do we expect looking forwards?

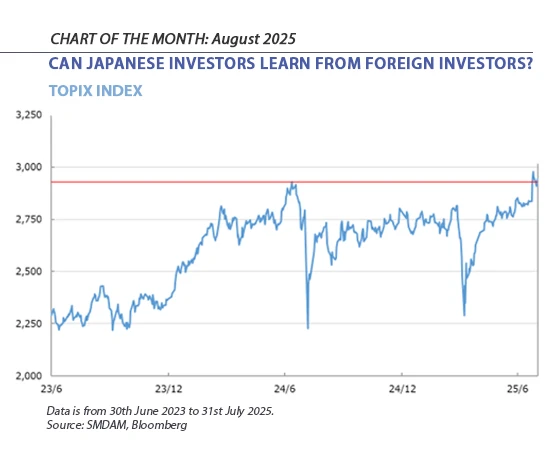

A year in the life of the TOPIX

As shown in the chart, the last 12 months have been something of a roller-coaster for the Japanese market with a combination of domestic and international factors behind the volatility.

With hindsight, we can see that the journey towards the recent feat of notching up a new all-time high began in the dark days of April, with the global economy reeling from the announcement of a dramatically more protectionist trade policy from the US. However, progress since then has been relatively steady, and the TOPIX saw a significant rise starting in late July triggered by the positive surprise of the sudden conclusion of the Japan-US tariff negotiations.

Too much of a good thing?

We have recently been cogitating on the potential long-term consequences of a sustained rise in asset prices for society.

In order to understand such dynamics, the work of Thomas Piketty is illuminating. Piketty has argued coherently in his book Capital in the Twenty-First Century that an extremely significant relationship in this regard is how the rate of return on invested capital stands in comparison to GDP growth rates. If the return to holders of capital is greater than broad economic growth, then wealth inequality must be increasing, and vice versa if the relationship were reversed.

Piketty has been one of the leading contemporary economists bringing attention back to such foundational issues, and his work has seldom been more relevant than today, with concerns about fairness and inequality now permeating many developed societies and driving political agendas.

The perspective this offers on contemporary developed economies is indeed a fascinating one. In the US, for example, the S&P 500 has increased approximately 18 times over the past 35 years; meanwhile, the average nominal wages of American workers have only risen about 3.17 times over the same period.

Over the same period, the MSCI ACWI has increased by about 7.8 times, and the NASDAQ has surged approximately 48 times. Therefore, it can be said that the continuous breaking of new all-time highs in the world’s stock markets is a common sight for many people around the world, albeit one that arrives at markedly different rhythms for different jurisdictions.

How does Japan compare?

Interestingly, the Japanese stock market differs substantially from this global stock market norm. Due to the highly atypical asset price surge in the late 1980s and the subsequent prolonged deflationary pressures on the economy, it took about 34 years for Japan's stock market to reach and pass its all-time high again in 2024.

In short, most Japanese investors active today simply have not seen this type of euphoric, momentum-driven market before. In contrast, active stock pickers in Japan survived the long, flat equity markets of the 1990s and 2000s by adopting a "range trading strategy," effectively selling when stock prices rise and buying when they fall. Rather than expecting a continuous if oscillating upwards movement of their index, the Japanese thus learn to invest a little along the lines of classical value theory, buying when cheap and selling when dear.

A new dynamic for the Japanese market?

For Japanese investors accustomed to such a "range trading" approach, paradoxically the bull market in Japanese stocks over recent years may not have been as positive as it appears. Japanese retail investors in particular have deeply adapted their buying and selling approaches to the markets where range trading worked well during the deflationary period. Consequently, they are often missing out on rapidly rising markets by focusing excessively on downside protection and taking profits too soon. Now that Japanese stocks appear to have established themselves on an upwards trajectory, this could be changing, however. With the uncertainty surrounding President Trump’s tariffs fading, there is a real possibility of a significant upward shift in both the trading range and of Japanese investors expectations of the market’s potential.

Half-full or half-empty?

When we turn to the market data, the 12-month forward EPS for the TOPIX hit a secular low at the end of June. Notably, this was just before the US-Japan tariff negotiations concluded, and since then the revised index of updated analyst forecasts, which had been significantly negative, is rapidly improving. Quarterly earnings reports show that corporate performance remains steady, although some export-dependent companies are lagging the rest of the market. Over the past decade, short-term speculative buying activity resulting it lofty valuations have often been justified by subsequent improvements in fundamentals and revisions in analyst earnings forecasts. We see this as a very real possibility again today.

Is the deflationary ghost still haunting Japanese investors?

More important for short-term market fluctuations is the presence of numerous investors who remember the deflationary era. These investors still tend to trim or entirely sell out of their positions hastily due to short-term market momentum. Such investors, facing a short squeeze in a rising market, could further amplify market volatility in the months ahead.

Considering that international investors reportedly account for about 60% of daily trading and about 30% of voting rights in Japanese equities, their choices and decisions are always closely watched by local market participants. In our view, Japanese investors could learn from their international counterparts by maintaining a stance of risk-taking and staying in a market that continues to achieve new highs, rather than being overly concerned with potential downside risks. As Japan moves further towards overcoming deflation, it is crucial to adopt an altered perspective towards the stock market – one which is able to look through short-term volatility to long-term upward trends

Risk warning: The figures refer to the past and that past performance is not a reliable indicator of future results. Performance is shown in JPY, the return may increase or decrease as a result of currency fluctuations.

Invest with us

If you have any account or dealing enquiries, please contact BBH using the following contact details:

Brown Brothers Harriman (Luxembourg) S.C.A.

80, route d’Esch, L-1470 Luxembourg

T: +352 474 066 226

F: +352 474 066 401

E: Lux.BBH.Transfer.Agent@BBH.com

Richard HAXE

Managing Director, Head of Business Development

Alex BARRY

Executive Director, Head of Distribution - UK and Ireland

Chloé CHOQUIN

Director, Business Development & Client Relations

Thomas CARTWRIGHT

Director, Business Development & Client Relations

|

Disclaimer An investment’s value and the income deriving from it may fall, as well as rise, due to market and currency fluctuations. Investors may not get back the amount originally invested. The information on this website is not intended to be investment advice, tax, financial or any other type of advice, and is for general information purposes only without regard to any particular user's investment objectives or financial situation. The information is educational only and should not be construed as an offer, solicitation, or recommendation to buy, sell, or transact in any security including, but not limited to, shares in any fund, or pursue any particular investment strategy. Any forecasts, figures, opinions or investment techniques and strategies set out are for information purposes only, and are based on certain assumptions and current market conditions that are subject to change without prior notice. The views of Sumitomo Mitsui DS Asset Management (UK) Limited reflected may change without notice. In addition, Sumitomo Mitsui DS Asset Management (UK) Limited may issue information or other reports that are inconsistent with, and reach different conclusions from, the information presented in this report and is under no obligation to ensure that such other reports are brought to the attention of any recipient of this report. Decisions to invest in any fund are deemed to be made solely on the basis of the information contained in the prospectus and the PRIIPS KID accompanied by the latest available annual and semi-annual report. |